Do Current Retirees Get More Out of Social Security Than They Put In?

Yes. Probably.

Yesterday, two of my readers—my mother and my grandmother on my stepfather’s side, whom we call Nonnie—were arguing about Social Security benefits. While my mother has long felt that Social Security should be means-tested, excluding people like Nonnie who are wealthy enough not to need the benefits, Nonnie believes she paid into the system, so she should get her money back. My mother’s contention was that she’s getting much more money out of the system than she paid in, but I wasn’t sure if this was true.

The general answer to this question has been covered by the Urban Institute, and depends greatly on the earnings of the individual in question. It also depends on the recipient’s gender, since women tend to live longer and collect more in benefits. In the table below, you can look at the Urban Institute’s estimates for various marital statuses, genders, and income levels. These are for those who retired in 2010; the numbers aren’t that different if you use 2015 instead. The most relevant figure, benefits minus taxes, is visible in the far right column.

In general, it looks like current Social Security beneficiaries are receiving more than they paid in, with two exceptions: those who hit the maximum for taxable earnings, and single males with high earnings. Another important and very interesting pattern to notice here is that the government shows a lot of favoritism to one-earner married couples, providing them with large benefits in excess of taxes paid.

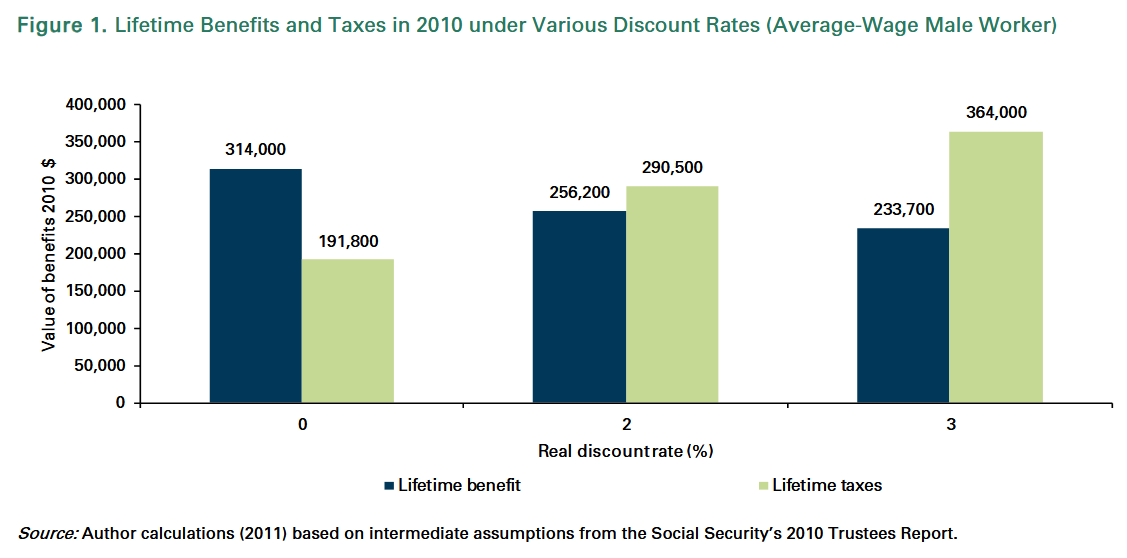

Urban Institute’s calculations are performed by adjusting past taxes for inflation and using an additional discount rate of 2%, comparable to what could be earned by investing in government bonds. They’re essentially comparing what a worker could have earned by investing their money in bonds to what they receive in benefits.

Most people don’t put all of their money in bonds, and could have easily invested their Social Security tax money in the stock market instead. That would make the system look much less generous to current recipients. These calculations are very sensitive to the discount rate used; if we change it to even just 3%—much lower than the S&P500’s average annual inflation-adjusted rate of return of over 6% a year since 1957—there’s a huge jump in the difference between benefits and taxes.

A potential complication I feared is the economic burden of taxes. On paper, it may appear that workers pay x% of their income in Social Security taxes, but part of that tax is passed to employers. Additionally, part of the employer match is passed to employees. The actual tax burden depends on the relative elasticities of labor supply and labor demand. Thankfully, the folks at Urban are professionals and state that they accounted for this in Appendix A.

But I think this entire exercise is a little silly. Social Security is not funded using money paid into the system in the past. It’s funded using money paid into the system now. More importantly, the value of Social Security benefits, like the value of all money, comes from what you can trade it for, which largely depends on the people who are working now rather than the people who were working in the past.

Just imagine a desert island with a group of 18-year-olds. They live and work there for their whole lives, and somehow they manage to not have any children. (The boys turned out to be a lot of sensitive young men who aren’t very good at dating.) If they develop money and save it, what happens when they’re all 65 years old and retire? The money is not magic. It cannot summon labor from the past. It becomes worthless once nobody is working and cannot provide the things people need to survive. If everyone retires and there are no children, everyone starves, so nobody retires (in this hypothetical, which I’m just using to make a point).

So in the real world, money collected in the past functions as a claim on wealth accrued over time, as well as services that have yet to be produced by the next generation. If the current generation of workers is smaller than the previous one—and it is—the system will be especially burdensome on them. It doesn’t matter all that much that current benefits are funded by current taxes, though that does make the nature of an elderly-slanted population pyramid more apparent.

I believe the relevant questions are these two:

What share of the typical worker’s income in the 1960s was used to pay for Social Security?

What share of the typical worker’s income is used to pay for Social Security today?

These two questions will tell us how burdensome Social Security was on Nonnie’s generation when they were paying into the system, and how burdensome it is on current workers. That should give us a better idea of how fair it is.

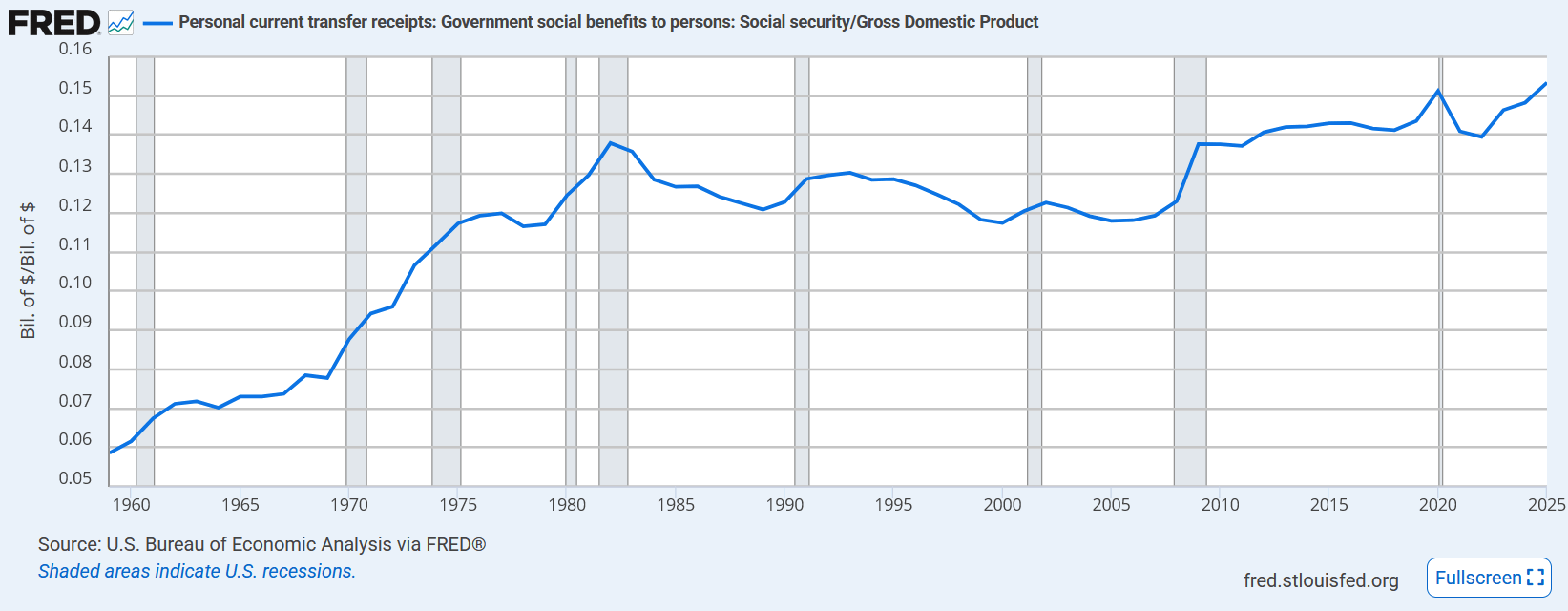

We could use the actual taxes paid in the 1960s and today, but I think that’s the wrong move. The right number to use is Social Security benefits as a percentage of all income, representing the burden of the system on the whole economy. That way, we won’t allow differences in government deficits and surpluses to influence our final result. The one thing we want to know is how much of the economy’s actual output is eaten up by Social Security payments. Unsurprisingly, this number has grown over time:

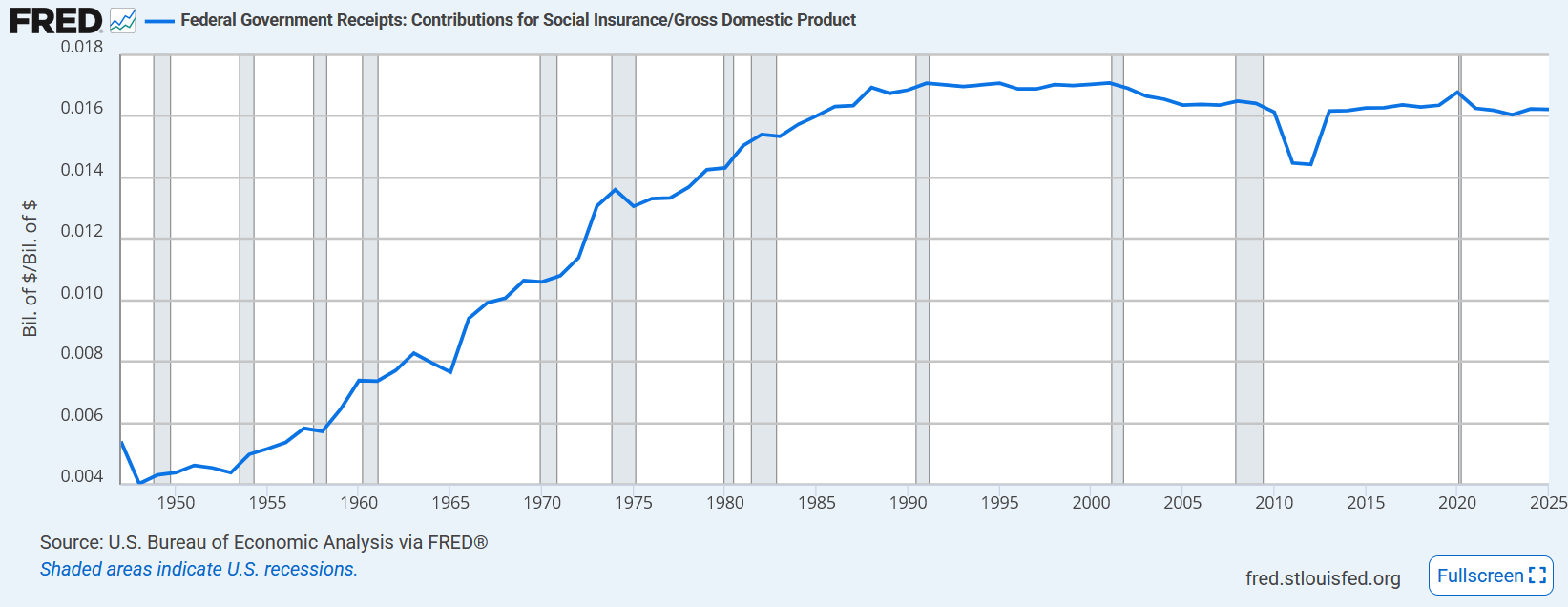

The picture is similar if you use taxes instead:

This tells us that early in the careers of the baby boom generation, the ratio of elderly dependents to working people was so low that it was hardly burdensome to fund Social Security. The system became much more burdensome over the course of their careers before becoming relatively stable in the 1980s. The biggest winners are probably people who reached the peak of their careers in the 1960s and are now long dead. Those reaching the peak of their careers right now, like Gen X, are huge losers of the current trajectory, though there’s still plenty of time to fuck over Zoomers as well.

To summarize: yes, Nonnie and other baby boomers are mostly receiving more in Social Security benefits than they paid in taxes. We’d expect them to get more if the system were “fair” since they were forced to forgo investment in higher-return assets like stocks. But current taxes fund current benefits, so the more important question is how burdensome the Social Security system was when you were working and how burdensome it is on people working today. From that lens, the system is massively unfair to people who entered the workforce after 1980.

I think the fundamental problem is that there’s a disconnect between how many children you personally have and how much you collect in retirement benefits. Returning to the desert island metaphor, if you choose not to have children and to just have more leisure time and consumption instead, you might be able to rely on everybody else to handle the child-rearing so that you have people to depend on when you’re retired. Your dollars are the same as anyone else’s dollars, and you get to keep more of them, so you get much of the benefit of other people raising kids even though you didn’t pay much of a price for that.

If each successive generation had as many kids as the previous one, things wouldn’t look so unfair. The general decline in fertility in the US is the source of the problem. Baby boomers don’t have as many grandkids as their own grandparents did, so the end result is that their early career didn’t have much of a Social Security burden, while the early career of Gen Z involves a much greater burden.

The problem could be solved by making a retiree’s claim on current output (in the form of Social Security benefits) at least partially proportionate to one’s contribution to creating the current workforce by raising kids. Why hasn’t such a solution been implemented? The losers of such a change would be current retirees who never had kids. In other words, a group of people with huge amounts of free time and very high rates of voter turnout. If you’re a politician, poking this group would be like sticking your head inside the mouth of a bear and holding up a sign that says “Please don’t eat me!” They call Social Security the third rail of politics for a reason.

The system does sort of have a way to deal with this problem. Remember how it shows favoritism to one-earner married couples? In theory, one would expect this kind of favoritism to essentially subsidize child-rearing and build the tax base needed for funding Social Security in the future: if you stop working to take care of kids, the government will treat you as if you are a current worker and provide Social Security benefits in the future. Clearly, this strategy has not worked.

Anyway. I don’t blame any individual for all of this happening, and I love all of my grandparents. I do not like the choice to make the system work this way. On the bright side, both my mother and Nonnie were kind of right, so they can both leave the conversation happy.

Ok Jack. My turn. You did an outstanding analysis of the value of Social Security, pros and cons.

When your mother and I had our discussion which, by the way, was very civilized, I was discussing this somewhat selfishly as my personal opinion whereas your Mom was viewing this from an altruistic point of view. Neither is wrong.

However, as I look at your first chart to see where Poppie and I fall, we definitely contributed more than we will collect as current retirees. I will take this as a win even though we lose. So be it.

Thanks Jack.

I'll take this as a win. I will also state that my central thesis, which was not included in your post, is that Social Security is an anti-poverty program, created to combat the devastating poverty exposed by the Great Depression, particularly among the elderly. The entire goal of social security was to provide a saftey net for old people who could not work and had no savings.

Today, the generation born between 1946 and 1964 (Boomers), have been the recipients of more government handouts than any other generation. They received 1) subsidized state funded university educations that are long gone, 2) had fully funded corporate pensions backed by federal law (also long gone), 3) could afford a home b/c of the GI Bill and no student debt (b/c they had low cost universities!), and 4) they have removed revenue (taxes) from the government b/c they don't want to pay for anyone else to have nice things.

We now have a $40TRILLION debt that will be passed on to their grandchildren only made worse by their guy, Trump.

My point is that wealthy Boomers don't NEED social security because they are clearly not living in poverty. And perhaps they could take a lesson from the greatest generation, their parents, and for once, make one sacrifice after bleeding the US and various state governments dry their entire lives.

And yes, I love you, Nonnie.

NOTE: I do not include Black Americans from most of this rant because they were excluded from many of these programs. Those Black Boomers can have whatever they want.